10 Money Saving Tips (that actually work)

Feb 07, 2026Read time - 4 minutes / Disclosure

Saving more money can:

- Lower your stress.

- Increase your savings.

- Grow your investments faster.

Unfortunately, costs keep going up.

Everyday Living

Today many people are stressed over:

- The cost of food.

- The cost of housing.

- The cost of insurance.

Hell, I've been worried about these things too.

Prices have been growing faster than usual.

Most people do their best to deal with it.

But there's only 2 options.

Option 1:

Make more money.

Option 2:

Save more money.

Not worrying about what other people think can also be helpful.

5 signs you're on track to escape

— JOHN HENRY (@thejohnhenry_) February 2, 2026

the 9-5 life early:

1. No car payment.

2. No credit card debt.

3. An emergency fund.

4. Investing every month.

5. Not caring what other people think.

When I was younger, I learned most of this stuff the hard way.

I had:

- Big car payments.

- Maxed out credit cards.

- Not much money saved.

And life was stressful.

The truth is..

It happened slowly.

One day at a time.

One small money decision after another.

And one day I woke up thinking...

"how the heck did I get to this place?"

I felt trapped in my job because of the money decisions I'd made.

It was a terrible feeling.

But working in finance helped me fix many of my bad habits.

Learning from people smarter than me.

Slowly fixing the financial mess I'd created.

And building better money habits into my life.

"Saving is the gap between your ego and your income."

— Morgan Housel

The Path Forward

Here's 10 money saving tips I learned the first 10 years I worked in finance.

Tips that completely changed my financial life.

Hope they're helpful.

Let's begin.

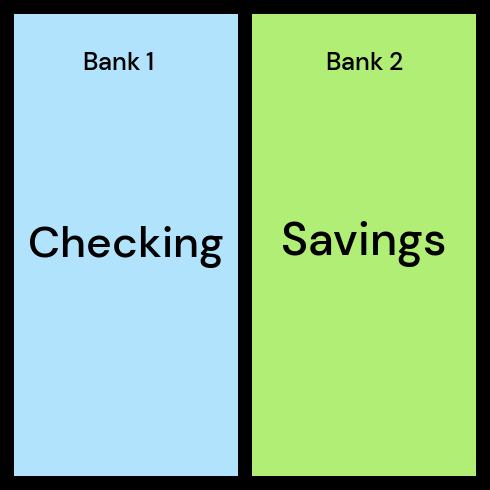

1. The Account Split

Most people have their checking and savings accounts at the same bank.

I did too for a long time.

But I eventually learned keeping them at different banks works better.

Transferring money between a checking and a savings account is easy..

..when they're at the same bank.

When they're at different banks..

..it's harder.

Which helped me save more money.

Keeping a savings account at a different bank than your main checking account can help you save more money.

2. The High-Yield Savings

Most people keep their savings account at a big bank.

But according to nerdwallet.

Most big banks pay 21 times less interest on their savings accounts.

Compared to opening a high-yield savings account.

For example:

$5,000 in a savings account at a big bank paying .02% interest

= $1.00 in 1 year

$5,000 in a high yield savings account paying 3% interest

= $150 in 1 year

A huge difference.

Using a high yield savings account can help you save more money than using a regular savings account.

3. The Auto-Pilot Hack

Most people plan to save and invest when they have "extra money".

That's what I thought too at first.

But life gets busy.

Things come up.

And before you know it..

5 or 10 years have passed.

I've found investing on auto-pilot is a better way to go.

Which means having part of each paycheck:

- Go into a savings account automatically.

- Go into a retirement account automatically.

- Go into an investment account automatically.

Instead of dumping each paycheck into a checking account and then spending the money.

Having each paycheck go into a checking account and a savings account and an investment account.

Most employers let their employees send their paycheck to 2 or 3 different accounts.

"Do not save what is left after spending, but spend what is left after saving."

— Warren Buffett

Saving and investing automatically (even if it's a small amount at first) helps you build wealth every time you're paid.

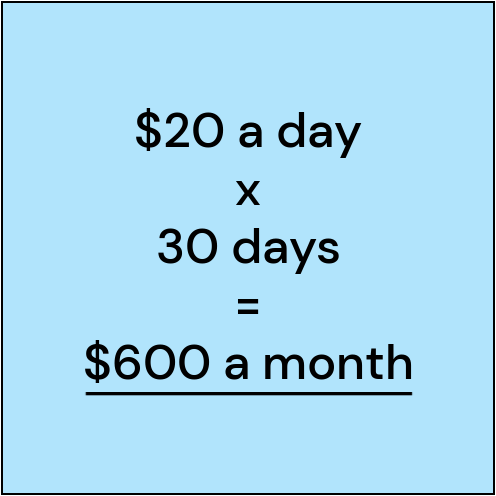

4. The 30-Day Rule

Most people spend money on smaller things every day without giving it much thought.

Things like:

- Coffee.

- A snack.

- A nice lunch.

- An afternoon snack.

- Dinner from a food delivery app.

But smaller daily spending on things can be very sneaky.

The 30-day rule can help.

It says to: "multiply each small daily thing by 30".

So if spending $20 a day on a coffee and lunch, it looks like this:

The 30 day rule helps you better understand how smaller daily spending on things affects your total monthly spending.

5. The Credit Card Hack

Most people make a payment on their credit card after receiving the bill.

But there's 2 perks I learned if paying my credit card before the bill comes.

Perk #1:

Setting a reminder on my phone to check my credit card every 2 weeks (every other Sunday).

And paying the bill off early.

I've found doing this makes it harder to accidentally spend too much money.

Perk #2:

Paying the card off before the bill comes means the credit card always shows up on my credit report as a $0 balance.

This helps my credit score and helps make getting loans easier (like a home loan)..

..since my credit card balance always shows as $0 on my credit report.

Setting a phone reminder to pay your credit card every 2 weeks instead of every month can help you avoid accidentally spending too much money.

6. The Authorized User Hack

Most people with low credit scores pay more money than people with high credit scores.

Credit scores have a huge impact on how much money we pay when:

- Renting an apartment.

- Getting insurance.

- Buying a home.

- Etc.

But the authorized user hack can help boost a low credit score.

For example:

Emma and Dan want to buy a home.

Emma has a great credit score.

Dan's credit score isn't so great.

Both Emma and Dan know his low score can affect the interest rate they get on a home loan and how much money they pay for insurance.

So Emma decides to add Dan as an authorized user to a credit card she's had for a long time that has a big credit limit and a zero balance.

Emma figures if adding Dan to her credit card doesn't help his credit score.

She can always go back and delete him as an authorized user.

So Emma logs into her credit card account online and adds Dan as an authorized user.

It takes 2 minutes.

Within 30 days, her old credit card she's had for a long time with a big credit limit and a zero balance shows up on Dan's credit report.

And his credit score goes up 80 points.

In finance, I've watched people do this over and over again.

The authorized user hack can be a quick way to boost a low credit score (but there's no guarantees it will work).

7. The 48-Hour Rule

Many people make big purchase decisions quickly.

Decisions like:

- Buying a car.

- Buying fancy jewelry.

- Splurging on a vacation.

I've done these things too.

But after discovering the 48-hour rule.

It's helped me spend less and save more money.

If often looks like this:

The 48-hour rule says: "wait a full 48-hours before buying an expensive thing".

I've found most of the time, the urge to buy the expensive thing passes.

The 48-hour rule can help you avoid impulse purchases and focus more on buying things you truly enjoy.

8. The Big Ticket Hack

Many people take the first offer when buying an expensive thing.

Things like:

- A car.

- A home loan.

- A new roof on their house.

But the big ticket hack can be a huge money saver.

It says: "get 2 estimates at the exact same time whenever possible".

For example:

I needed a new hot water heater a few months ago.

I scheduled 2 companies to come out and give me an estimate at the exact same time.

Both of the guys sat in their trucks waiting for me to make a decision after providing their estimate stating they'd each "give me the best deal".

In the end, one company was $500 cheaper than the other.

The big ticket hack forces companies to compete for your business which can save you a lot of money.

9. The Insurance Hack

Most people quickly setup an insurance policy when needed and don't think about it again.

Many years pass before they start to wonder..

"Am I paying too much money for that insurance?"

So they shop around and spend hours comparing different insurance quotes before switching to a new company.

I've been there too.

It can be a pain.

But one day my friend that works in insurance told me about the insurance hack.

And explained: "instead of spending hours getting quotes from individual insurance companies, just use an insurance broker".

So I switched all my insurance policies to an insurance broker 10 years ago.

Most insurance brokers have access to 30+ different insurance companies.

That means with one quick call every couple years.

The insurance broker can easily shop insurance rates for me, cancel my current policies, and switch me to a different insurance company with better pricing if available.

I've found it to be a lot easier.

And doesn't cost me any extra money.

Using an insurance broker can save you time and money (google "insurance broker" + "your city" to find them).

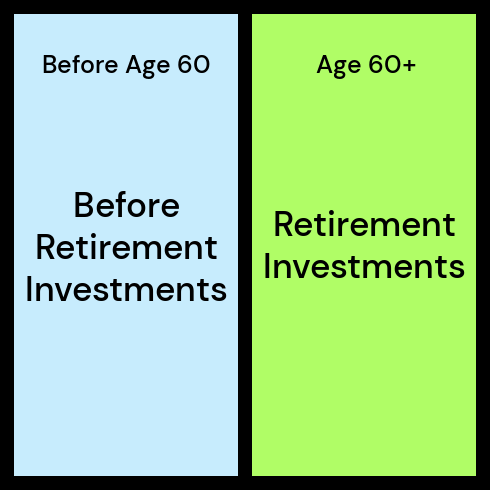

10. The Retirement Short Cut

Most people save and invest most of their money in a retirement account.

That's exactly what I did starting off.

But then one day I realized most of the people I worked with in my finance job that retired early..

..didn't just have retirement investments.

They also had "before retirement investments".

They didn't want to wait until their 60s to leave 9-5 life.

So they setup their investments in two different ways:

So I started focusing more on my "before retirement investments".

Which meant also investing in a non retirement account (they're often called a "self directed investing account".)

Having before retirement investments can help make leaving 9-5 life early much easier (if you want).

The bottom line

Most of the people I've met that left their 9-5 job decades early to live their ideal life had a playbook.

A playbook of tips, hacks, rules, or habits to help keep them on track.

Habits that helped them:

- Save more money.

- Invest more money.

Not to impress people.

Not to buy a fancy car.

Or fancy clothes.

But to buy back their time.

To have the option to leave 9-5 life early.

To do their own thing.

To see their family more.

To work part time on something they truly enjoy instead of spending 40 years at a 9-5 job feeling stuck.

I hope this little list of money saving tips is as helpful for you as it's been for me.

Thanks for taking the time to read it.

That's all for today.

See you next Saturday.