5 Steps to a Lower House Payment (when buying a home)

Jun 06, 2026Read time - 4 minutes / Disclosure

Having a lower house payment can:

- Save you money.

- Make you money.

- Free up extra cash to invest.

Unfortunately, living costs keep rising.

The Numbers

Over the past 5 years, according to the U.S. Census Bureau:

- The average house payment has increased by 40%.

- The average rent payment has increased by 30%.

...which is a harsh reality.

And what if you want to make a change?

To go from renting a home to buying a home.

What would the monthly payment actually look like..

And what could you do to keep the payments as low as possible?

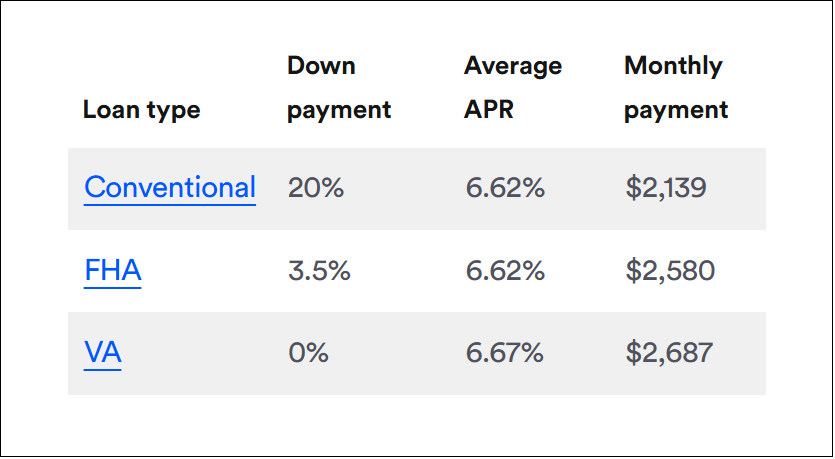

Here's a monthly home loan payment estimate from Bankrate before taxes, insurance and other costs for a $417,700 30-year home loan:

Bankrate estimate

When getting a loan to buy my first home, I thought a lot about 2 things.

1. How much money do I need to make it happen.

2. How do I make sure to have the lowest monthly payment possible.

After looking into it more.

I learned America has the most flexible home loan programs in the entire world.

Some loan programs don't even require a down payment.

And other loan programs only require a small down payment.

And many programs offer a 30-year fixed rate home loan.

Things that are unheard of in many other parts of the world.

But I was worried if I put down a smaller down payment.

I'd have a larger monthly payment.

And going from paying rent every month to paying a mortgage every month is a big jump for most people.

The mortgage payment for a first time homebuyer can be $500 or $1,000+ more per month than a rent payment.

"More important than the will to win, is the will to prepare."

– Charlie Munger

After learning my monthly payment would be a lot more.

I still wanted to become a homeowner.

But I needed to figure out a way to keep my monthly payment down.

To avoid spending everything I earned on a home.

And the only thing I could come up with at the time..

Was to buy a home with extra space I could rent out.

I noticed buying a 2 bedroom condo wasn't much more expensive than buying a 1 bedroom.

So I took the plunge and got a loan to buy a tiny 2 bedroom condo as my starter home.

And rented out the 2nd bedroom to a friend.

Receiving rental income helped make going from renter to homeowner a little bit easier for me.

The "Lower House Payment" Checklist

Over the next decade, after getting loans to buy 6 more properties.

I learned more ways to lower the house payment when getting a loan to buy a home (besides having a renter).

Here's 5 more ways to consider.

Let's dive in.

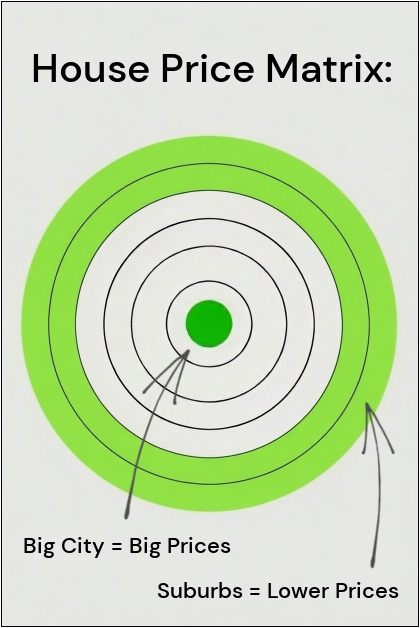

1. The Location

Compare several neighborhoods.

Why?

Because location changes everything when shopping for a home.

Especially the price.

According to realtor (dot) com, homes in the suburbs are 23% less expensive than homes in the urban city core on average.

Choosing to buy a home 15 to 30 minutes from a bigger city can save you $100,000+ on the purchase of a home.

2. The Insurance

Shop several insurance companies.

Why?

Because buying a home means needing homeowner's insurance.

And just like car insurance..

The price of homeowner's insurance varies.

A $200 monthly homeowner's insurance policy with one company.

May cost just $80 a month with another.

Spending an hour shopping for homeowner's insurance on your new home can save you hundreds or thousands of dollars per year.

3. The Assumption

Ask if the seller's mortgage loan is assumable.

Why?

Because if the person selling their home has an assumable mortgage.

It can a huge way to save money.

How?

Assuming a seller's mortgage loan means:

The seller's mortgage company takes the home loan out of the seller's name.

And puts the home loan in the new homebuyer's name.

But why would a homebuyer do this?

Because the seller of the home may have a lower interest rate on their loan (a lower rate than is available today).

For Example:

Let's say James gets a home loan pre-approval to buy a home.

And he finds out the interest rate on his new home loan will be 6%.

And a month later he finds the perfect home.

After asking if the seller's mortgage loan is assumable..

He finds out the seller has owned their home for 5 years, their home loan is assumable and the seller's interest rate on their loan is only 3%!

If James decides to take over the seller's home loan, the interest rate on his loan would be 3% instead of 6%.

Taking over the seller's loan means James would have a lower monthly payment.

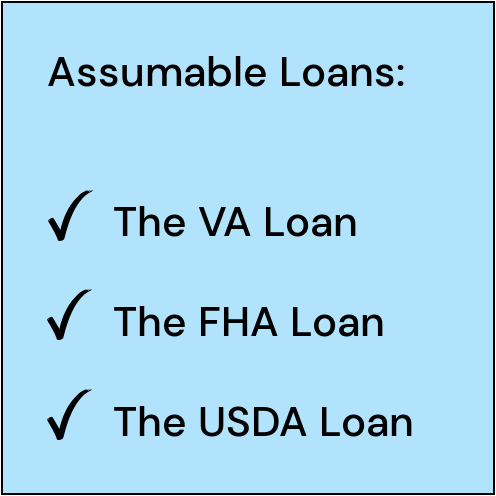

Not all home loans are assumable.

Here's a few that are:

Here's a few more things to know:

1. James must apply to take over the seller's loan directly through the seller's lender (the company that sends the seller their monthly home loan statements). And James must qualify to take over the monthly payment.

2. James will likely need to get a 2nd loan as well. Why? For example: If the seller agrees to sell James their home for $400,000 and the seller's loan James is taking over is just $300,000- James needs to get a 2nd loan for the difference.

So..

If $400,000 is the sales price.

If $300,000 is the loan James is taking over.

James needs to come up with the difference of $100,000 as well.

James can use cash to cover the $100,000 if he has money saved, get a 2nd loan or do a combination of both things.

This many sound a bit confusing.

But the good news is..

James's real estate agent will help him figure these things out if he finds a home with an assumable mortgage he wants to take over.

Assuming a home seller's low interest rate mortgage loan can save you thousands of dollars in monthly home loan payments.

4. The Down Payment

Put down a bigger down payment.

When getting a loan to buy a home.

The larger the down payment a homebuyer has.

The lower their monthly home loan payment will be.

The most common places people find down payment money include:

- Checking/savings.

- Investment accounts.

- Gift funds from family.

- First time homebuyer programs (the average first time buyer program provides $18,000).

Putting down a larger down payment when buying a home (if possible) means you have a smaller mortgage loan and a smaller monthly payment.

5. The Interest Rate Hack

Consider buying down the interest rate.

What does this mean?

For Example:

If James's decides not to assume the seller's mortgage (mentioned earlier).

And wants a lower interest rate on his home loan then the 6% rate his lender offered.

He could tell his lender he wants to "buy down" his interest rate.

What does this mean exactly?

Buying down the interest rate means choosing to pay extra money up front to get a lower interest rate.

After James tells his loan officer he wants to "buy down" his interest rate.

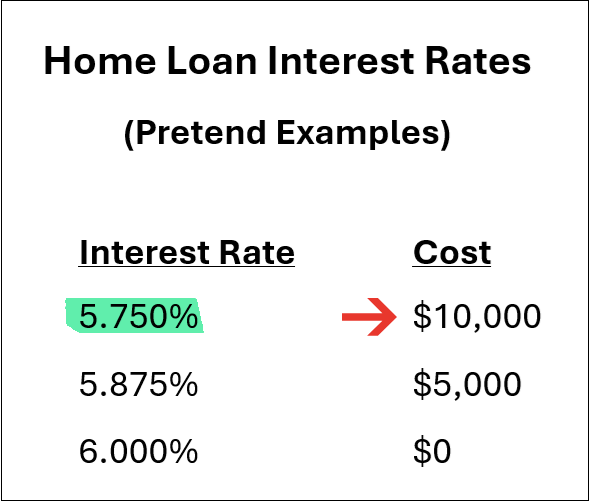

The loan officer may give him a few options that look like this..

Example

In this example, if James wants the lower 5.750% interest rate so he has a lower monthly home loan payment.

He would need to pay an extra $10,000 to his home loan lender when closing on his new home.

But what if James doesn't have an extra $10,000 laying around (I sure didn't when buying my first home).

The good news..

The $10,000 doesn't have to be paid by James.

It can be paid by someone else, like the home seller.

James and his real estate agent could negotiate with the home seller by asking for a $10,000 credit.

And if the seller agrees, James could use that credit to get the lower interest rate without having to pay for it himself.

Choosing to buy down your interest rate can lower your monthly home loan payment (and someone else can pay for all or part of it on your behalf).

The bottom line

Going from having a rent payment to having a house payment can be scary.

Renting out part of my very first home helped give me the courage to take out my very first home loan.

I still remember feeling intimidated while signing the loan papers at the very end 20 or 30 times.

And wish I'd discovered these other ways to save money when buying a home much sooner.

If you see buying a home in your future.

Or maybe buying a rental property.

I hope these 5 ways to save money on a house payment are helpful on your journey.

That's all for today.

See you next Saturday.