7 Homebuying Traps (with examples)

Aug 09, 2025Read time - 4 minutes / Disclosure

Owning a home can:

- Settle your family.

- Boost your net worth.

- Create generational wealth.

Unfortunately, there's many traps to avoid.

Homebuying Blunders

Making mistakes along the way can cost you:

- Time.

- Money.

- Your sanity.

But mistakes are part of the homebuying journey.

Avoiding them (and homebuying altogether) could mean missing out on wealth building as an owner.

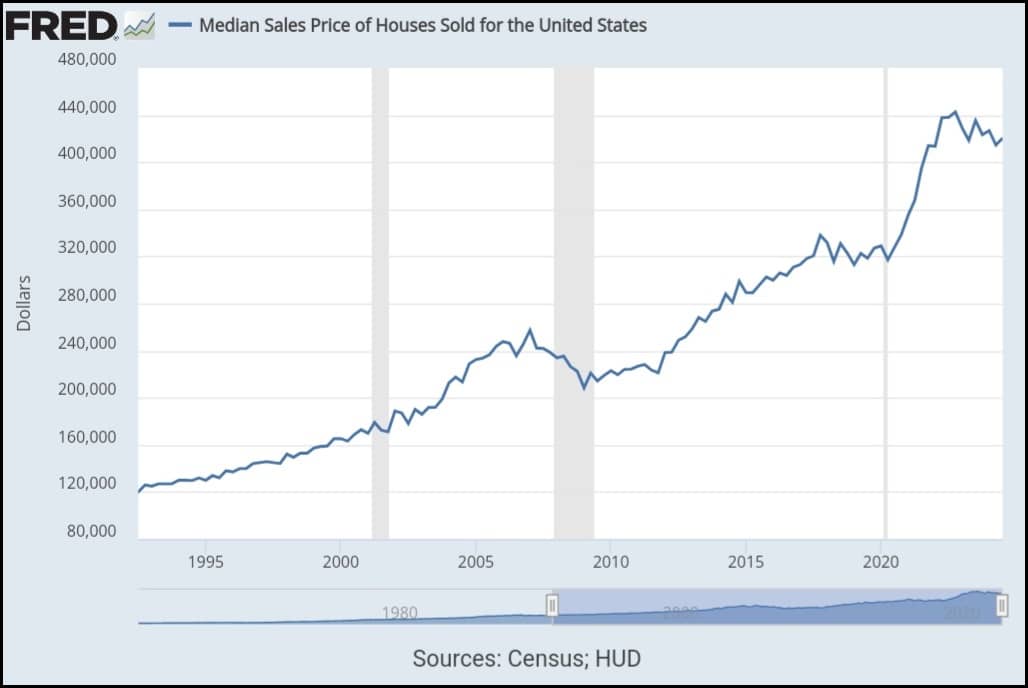

30yrs of home prices

Although homebuying isn't for everyone.

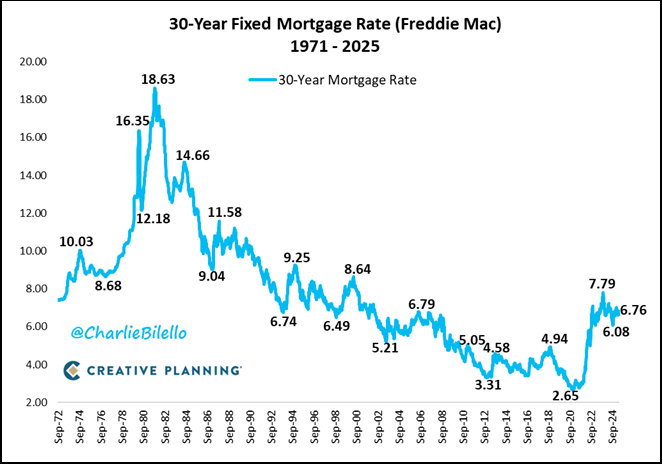

I think it will become easier as interest rates start to fall again.

50yrs of interest rates

Figuring out how to buy 7 properties starting from scratch.

And helping 1,000+ people navigate homebuying while working at Chase helped me identify many traps.

Traps I've fallen into myself.

The "Homebuying Blunders" Checklist

Here's 7 homebuyer traps I've learned the hard way (hope it's helpful).

Let's dive in:

1. The Inspection

Skipping a home inspection can be painful.

Home inspections uncover:

- Roofing problems.

- Electrical problems.

- Plumbing problems.

...plus much more.

These issues can be negotiated with the seller before you buy their home (if you know about them).

For example:

Several years ago I knew a guy that bought a home in Florida.

He skipped his home inspection.

Upon moving in, he found hundreds of cracks in the flooring throughout the home. The seller covered up the cracks with rugs.

It's likely a home inspector would have found them.

Spending a few hundred dollars on a home inspection can save you thousands.

2. The Escape Plan

Waiving contingencies can be costly.

A "contingency" is a fancy sounding term that means:

A future event or circumstance that can't be predicted.

For example—

Your offer to buy a home is accepted.

But afterwards, you find out:

- The roof is bad.

- The electrical is bad.

- The plumbing is bad.

Contingencies let you change your mind about buying a home (they're your escape plan).

Real estate agents can include contingencies in your homebuying offer to protect you.

3. The People

Inexperienced people can sting.

Over a decade ago.

I made my first offer on a property.

My friend who just got his real estate license wrote up the offer.

The seller accepted my offer and I put down a $1,000 deposit.

Unfortunately, the deal didn't work out.

But my friend (the new real estate agent) didn't include any contingencies in my offer.

So I lost my $1,000 deposit because I didn't have an escape plan.

(I also didn't know what the heck a contingency was)

Working with experienced people can help save you time and money.

4. The Ego

Flexing an ego can be painful.

I've watched hundreds of people submit offers on their dream home.

Many got it.

But several lost out due to ego.

Here's an example:

A buyer offers $370k on a home.

- The seller asks $390k.

- The buyer offers $375k.

- The seller asks $385k.

- The buyer offers $380k.

The seller takes a different offer.

This happens a lot.

Although negotiating is part of homebuying.

Many deals fall apart over a few thousand dollars.

Every $5,000 added to a home loan is roughly $32 in the monthly payment.

Negotiating with an ego can lose a home, breaking down the difference when deciding is helpful.

5. The Peanut Gallery

Not everyone's opinion matters.

When you're a homebuyer, everyone comes out of the woodwork to give you advice:

- Your aunt.

- Your sister.

- Your parents.

- Your 3rd cousin.

I've seen a lot of people miss out on their ideal home because of listening to someone's unsolicited advice.

Listening to professionals is a better strategy.

But don't forget, most professionals get paid after you buy a home not before.

(you buying generates commission)

Keep that in mind too.

Listening to experienced pros help increase your odds of homebuying success.

6. The Pre-Approval

Loan pre-approvals aren't a guarantee.

A pre-approval is an educated guess by a loan officer that your homebuying application will be approved.

Your loan application isn't "fully approved" by a loan underwriter until a seller agrees to sell you their home.

So hold off on:

- Moving plans.

- Job transfer plans.

- Furniture buying plans.

....until your loan application is "fully approved" by a loan underwriter (usually 7-14 days before you close on your new home).

Waiting for your loan application to be fully approved can save you time and money.

7. The Special Programs

There's 2,000+ special homebuyer programs.

Programs that offer:

- $5,000

- $10,000

- $20,000+

...towards your new home.

But not all loan officers work with these programs.

Looking into special homebuyer programs can help you own a home much sooner.

The bottom line

There's a lot to homebuying.

And a handful of traps to avoid along the way.

The key is to avoid as many as you can by knowing what to look for.

Lord knows I've learned most the hard way.

But homebuying is a worthwhile journey — if you see it in your future.

Picking a real estate agent with loads of experience helps make it more enjoyable.

(and using one of the 2,000+ special homebuyer programs)

You can read reviews and find a real estate agent at realtor.com

You can find special homebuyer programs at fanniemae.com

That's all for today.

See you next Saturday.