How to Buy an Affordable Home (without much money)

May 16, 2026Read time - 4 minutes / Disclosure

Learning how to buy an affordable home can:

- Save you money.

- Make you money.

- Help you build generational wealth.

Unfortunately, many people have given up on homebuying.

The Problem

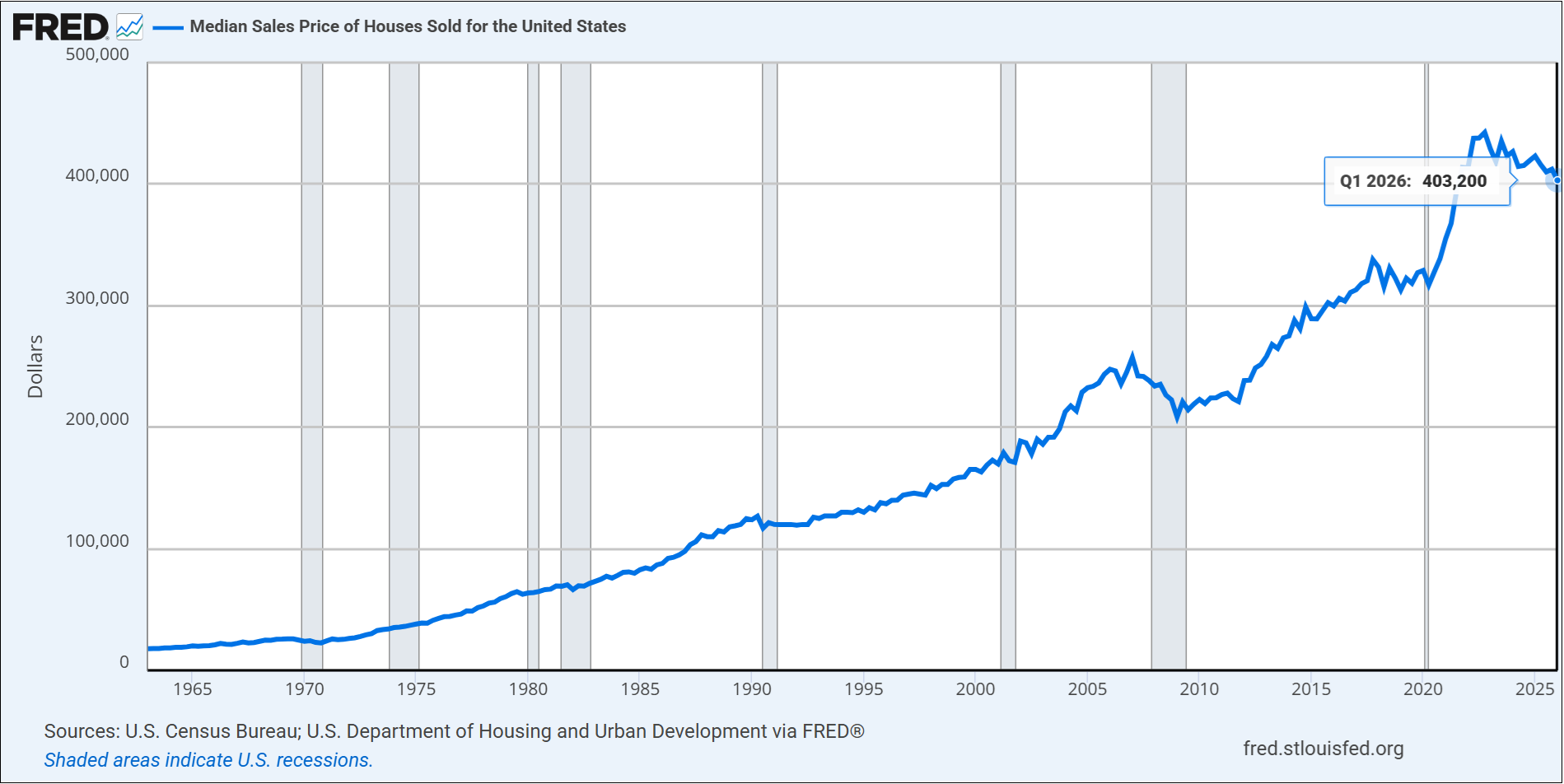

Over the past 5 years, according to the United States Federal Reserve:

- Home prices are up 22%.

- Insurance prices are up 30%.

And home loan interest rates have doubled.

A harsh reality for hopeful homebuyers.

Leaving many people to wonder..

Will I ever be able to afford a home?

The history of home prices

Buying my first home was a scary thing.

But after years of renting and having up to 5 roommates.

I decided it was time to see if I could get a loan to buy my first home.

It was exciting.

And stressful.

Things went faster than expected.

And a few months later I found myself owning a tiny condo near Seattle, Washington without having to come up with much money (around $1,500 bucks total).

My friend moved in and rented out the 2nd bedroom.

So I didn't have to pay the entire monthly payment all by myself.

Over the next two years that tiny condo went up $100,000 in value.

I was shocked.

And quickly found myself obsessed with real estate over the next decade:

- Getting loans to buy 6 more properties.

- Working at a bank helping other people get loans.

- Teaching over 40 first time homebuyer seminars for the bank.

"Buy land, they aren't making it anymore."

– Mark Twain

But my homebuying journey wasn't always easy.

I've made lots of mistakes along the way.

Mistakes I wish I knew how to avoid.

After leaving my banking job.

And starting this little online education business.

Many people have asked how I'd go about buying an affordable home today (without much money).

So here's exactly what I'd do starting from scratch.

The Affordable Home Framework

Two things I like to obsess over when buying a home include:

1. How to spend the least amount of money.

2. How to have the lowest monthly payment.

Here's the 5 steps I've learned to follow to help achieve these things.

Let's dive in.

1. The Payment Hack

According to the National Association of Realtors.

91% of first time homebuyers get a loan to buy a home.

But how the heck do you make sure the monthly loan payment is something you can actually afford?

I've learned the property type makes a huge difference.

The Condo

Many first time buyers choose to buy a tiny condo in a big building.

It's exactly where I started.

But buying a 2 bedroom condo can have lower monthly costs than buying just a 1 bedroom condo.

Let me explain..

A 1 bedroom condo often means making the entire monthly loan payment all by yourself (unless you have a significant other).

A 2 bedroom condo allows for rental income (if you don't mind renting out the 2nd bedroom).

Buying a 2 bedroom condo and renting out the 2nd bedroom often results in having lower monthly costs than buying a 1 bedroom condo and making the entire monthly payment all by yourself.

It's worth running the numbers and comparing both options.

But what if you don't want to have a roommate?

The House

Certain types of houses also allow for rental income to help lower your monthly costs (without having to share a kitchen or a bathroom with a roommate).

For example, a house with:

- A small livable unit in the backyard.

- A mother-in-law unit upstairs with a separate entrance.

- A garage converted into a living space with its own entrance.

Finding houses like this take a bit more work.

But can be a huge money-saver.

Choosing a property type that allows for rental income can lower your monthly costs by 25% to 40%.

2. The Homebuyer Money

Most people think they need to save lots of money all by themself to buy a home.

I also thought this at first.

But I eventually learned you can get $10,000 or $20,000 or even $30,000 to help you buy a home.

And the money can come from many different places like:

- The Program: Many first time homebuyer programs offer up to $18,000 on average to first time buyers.

- The Seller: A home seller can help pay part of your homebuyer costs.

- The Lender: A home lender can offer homebuyer credits that help cover part of your homebuyer costs.

- The Agent: A real estate agent helping you buy your home can offer part of their commission to help cover part of your homebuyer costs (if they agree).

To see exactly how this works you can find my free homebuyer money playbook here.

Having a plan to get homebuyer money can save you thousands of dollars and help you buy a home sooner.

TIP: Consider the property type you want to buy and the homebuyer money you plan to get before doing your home loan pre-approval.

3. The Pre-Approval

Do your home loan pre-approval with at least 2 different lenders.

Make sure each lender knows you're "shopping around".

Letting them know you're "shopping around" means they're more likely to offer you better deals like a lower interest rate to win your business.

It's also important to share with your lender any homebuyer money you're planning to get.

Because getting $10,000 or $20,000 or $30,000 in homebuyer money makes a massive difference when your lender is figuring out how much of a home loan you may qualify for.

Any homebuyer money you get can also be used to "buy down your interest rate".

Which means having a lower interest rate (and having a lower monthly payment).

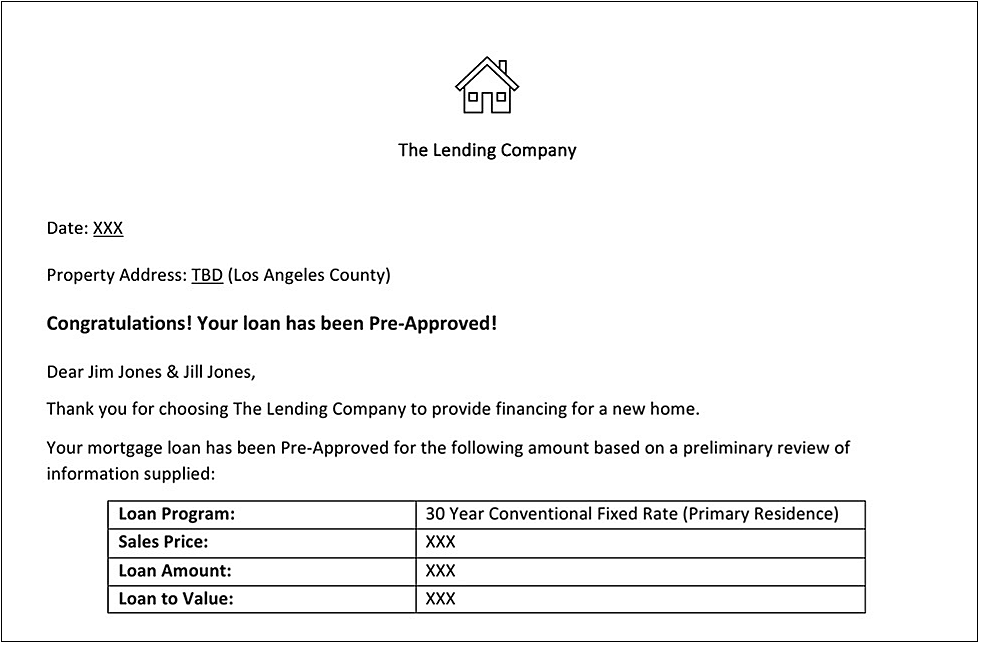

After reviewing your information, the lender will give you a home loan pre-approval that looks something like this:

Example pre-approval

Getting a home loan pre-approval with at least 2 different lenders and sharing your plans to get homebuyer money can help you get a better deal on a home loan.

4. The "What If Game"

Sometimes home loan pre-approvals come back just right.

For example:

- You asked for a $400,000 home loan pre-approval.

- And you got a $400,000 home loan pre-approval.

And other times, they don't:

- Maybe you asked for a $400,000 home loan pre-approval.

- And you just got a $300,000 home loan pre-approval.

When a pre-approval doesn't come back as expected.

One thing you can do is to play the "what if game".

It's a game I've played many times.

And it often looks like this..

Asking your lender different questions like:

- What if I paid off my car early?

- What if I paid off my credit card?

- What if I took a better paying job?

- What if I add a relative to my loan?

- What if I refinance my student loans?

Playing the "what if game" with your lender can help you identify a path to get the home loan pre-approval that you want.

5. The "Re-Approval"

After reviewing your options and making changes to your finances.

Maybe it takes a few days.

Maybe it takes a few months.

You can ask your lender to "re-approve" your home loan based on the changes you've made.

A helpful thing to know about home loan lenders is:

Many of them work on commission.

(I used to be one of them!)

Many home loan lenders only get paid when you get a home loan.

Which means many of them are happy to help you figure things out.

Even if it takes a few days, a few weeks or a few months.

Working closely with a home loan lender can help you figure out how to buy a home sooner.

The bottom line

Homebuying can be a confusing thing.

Especially the first time.

I've sure made my fair share of mistakes.

Things like:

- Not exploring how to get homebuyer money.

- Not getting a home loan pre-approval from 2 different lenders.

- Not playing the "what if" game to help increase my home loan pre-approval amount.

Things I've slowly figured out after working in banking and getting a loan to buy that first tiny condo.

I hope sharing what I've learned helps save you time and money if you ever decide to buy a home now or sometime in the future.

That's all for today.

See you next Saturday.