The 6 Things in a House Payment (and how to save money)

Feb 21, 2026Read time - 4 minutes / Disclosure

Knowing how a house payment works can help you:

- Pay less interest costs.

- Pay less insurance costs.

- Save you a lot of money.

Unfortunately, it can be a confusing thing.

The Monthly Bill

Most people looking at their monthly home loan statement see things like:

- Impound account.

- Principal payment.

- Primary mortgage insurance.

Words and phrases that might sound unfamiliar.

Most people assume the bill is right.

Send in the money.

And life goes on.

But making sense of a monthly home loan statement can lead to unexpected savings.

"Think of saving as earning."

— Andrew Carnegie

A month after getting a loan to buy my first tiny home.

I got my home loan statement in the mail.

Looking through the bill confused the heck out of me.

But I assumed it was right.

And made the payments.

10 years later I found myself doing loans at a bank for other people.

After looking through thousands of home loan bills.

I finally learned how to make sense of them.

And the different ways to save money.

House Payment 101

Here's the 6 things in a monthly house payment (and how you can save money).

Hope it's useful.

Let's begin.

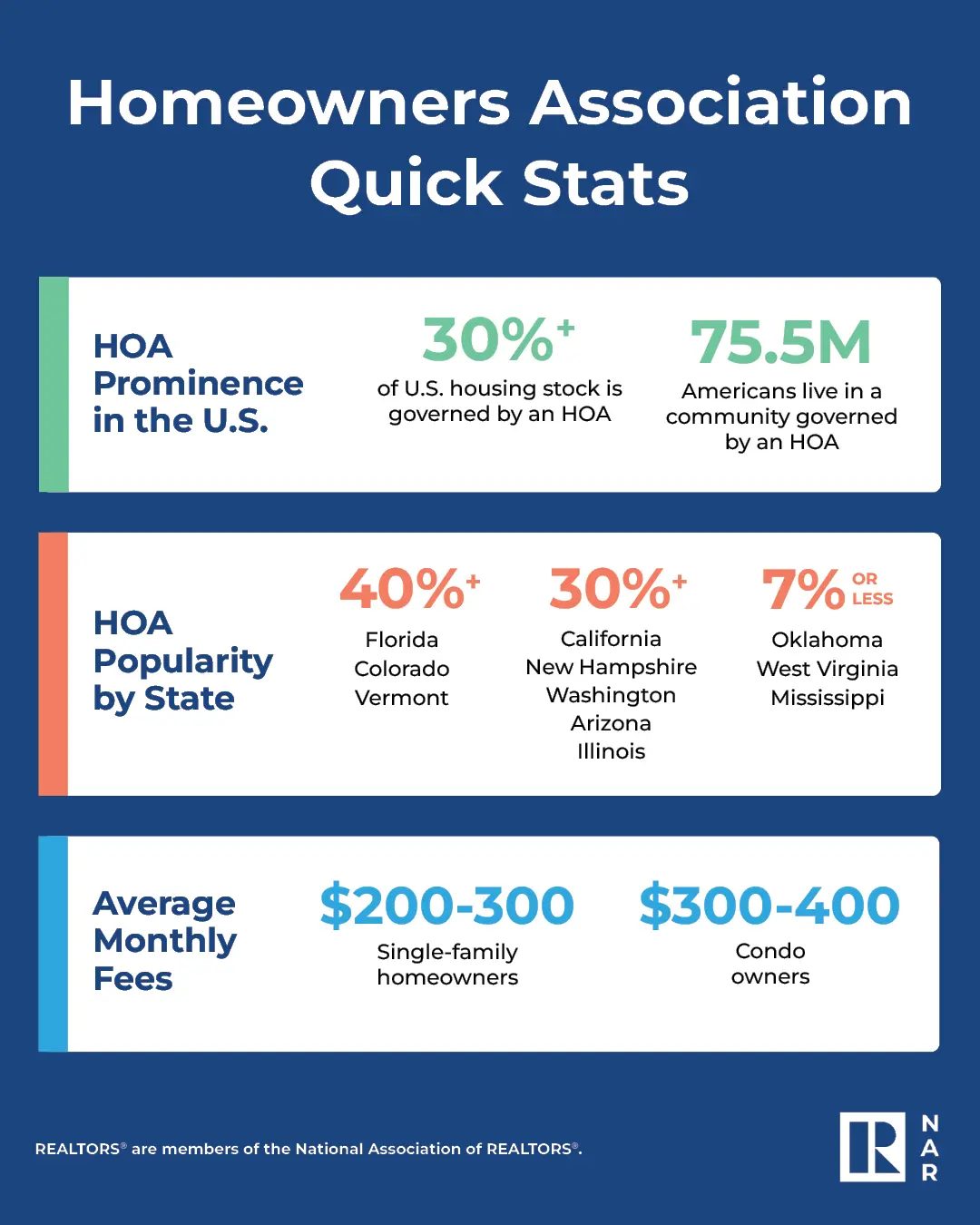

1. The Association

Many homes are part of an association.

They're also called HOAs.

Which stands for Home Owners Association.

Think of it like a mandatory membership.

Something you must become part of if you buy a home in a certain neighborhood.

For example.

My first home was a tiny condo.

It was part of an association.

So I had to pay a few hundred bucks every month to the condo association.

That payment included my monthly:

- Water costs.

- Sewer costs.

- Garbage costs.

So I didn't get a separate bill for those things.

And the condo complex had a pool and a little gym.

The monthly association payment helped maintain those things.

Houses and townhouses are sometimes part of an association too.

Association dues are a monthly payment you must make if you choose to own a home in a neighborhood that's part of an association.

2. The Insurance

According to Progressive, most people pay around $200 per month on average for their homeowners insurance.

Sometimes more, sometimes less depending on where you live.

And getting a loan on a home means you must have insurance.

Homeowners insurance covers things like:

- Stolen property.

- Damage from a fire.

- Injuries on your property.

Most people with cheaper homeowners insurance I've found, often have 2 things in common:

1. They get their home and car insurance from the same company.

It's called "bundling" your policies. Many insurance companies offer a discount if you have your home insurance and car insurance with the same company.

2. They have a good credit score.

Many states allow insurance companies to use your credit score when deciding how much to charge you for insurance.

So having a credit score above 700 can be helpful.

Bundling your insurance policies with the same company and having a good credit score are 2 ways to help lower your homeowners insurance costs.

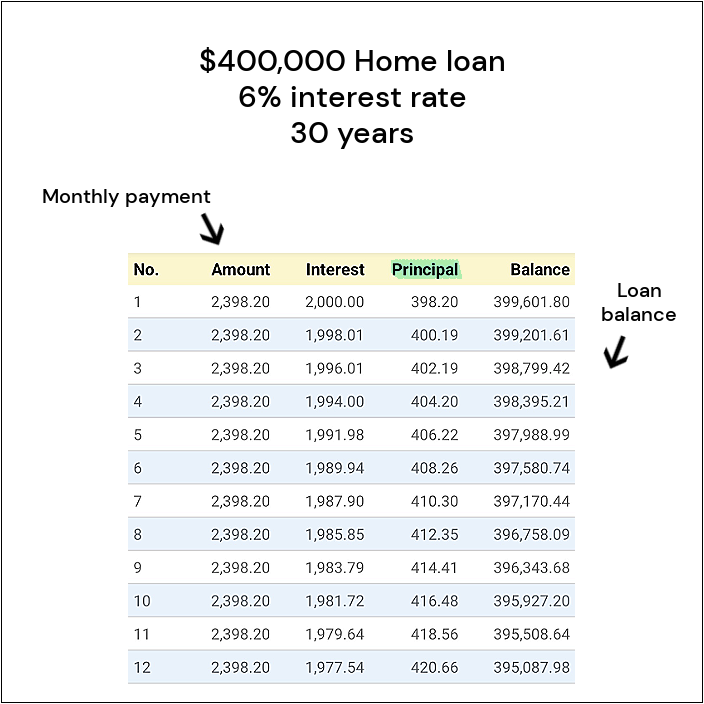

3. The Principal

With most home loans, every monthly payment you make helps lower the balance owed on your loan.

For example:

See how part of each monthly payment goes towards the "principal" in this example?

Example

Money going towards the principal of your loan every month helps you pay off your loan.

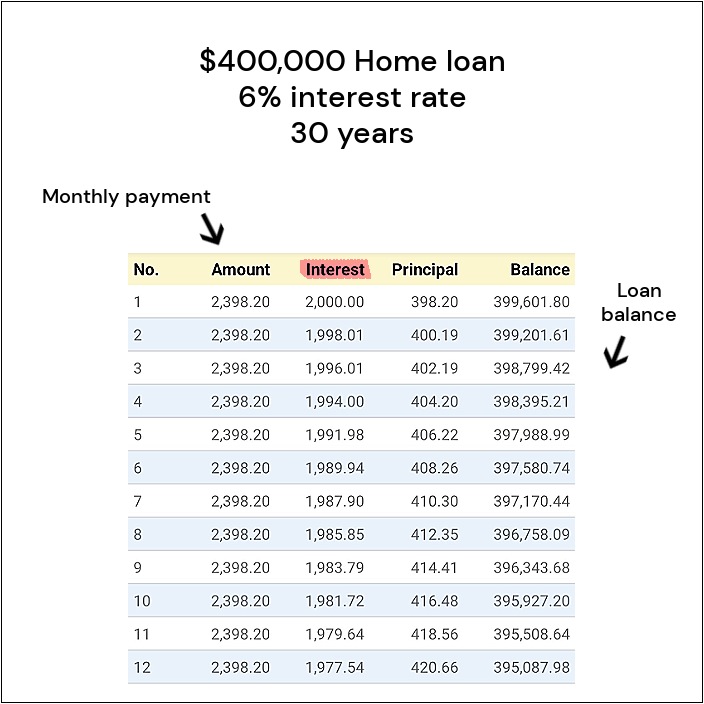

4. The Interest

Monthly interest paid on your loan is another monthly cost.

For example:

See how part of each monthly payment below also goes towards the "interest"?

Example

Notice how with every payment made, less money goes towards the interest and more money goes towards the principal?

One hack to pay less interest over the long run.

Is to make an extra principal payment each month.

In this example.

Here's what happens if making an extra $100 payment every month:

Example

An extra $100 every month saves an extra $55,758.08 in loan interest over the long run.

And pays off the home loan 36 months early (3 years early).

Here's the free calculator app I like to use when running these examples if you want to run your own little experiments:

Making an extra principal payment every month can help you save money on interest and help you pay off your home loan faster.

5. The Taxes

Owning a home means paying property taxes.

According to the National Association of Homebuilders, property taxes average $350 per month.

Sometimes more, sometimes less depending on where you live.

Fortunately, most people's property taxes are included in their monthly home loan payment.

And most people's homeowners insurance is also included in their monthly payment.

(unless your home loan lender lets you pay them separately on your own)

Once per year your home loan lender will adjust your monthly home loan payment as your property taxes and homeowners insurance costs change.

6. The PMI

Many first time homebuyers also have a monthly charge listed on their home loan statement called PMI.

Which stands for Private Mortgage Insurance.

When you get a loan to buy a home.

And you don't have a lot of money to put down (like me when buying my first tiny condo).

PMI is an extra charge that's often added to your monthly payment.

It can cost you anywhere from $100 to $300 per month on average.

PMI is "extra insurance" that protects the lender making your home loan.

But the good news..

You can get rid of PMI as the value of your home goes up.

And the balance owed on your home loan goes down.

I've seen people get rid of PMI in as little as 2 years after getting their home loan.

Unfortunately, many people forget they can cancel their PMI and keep paying for it longer than they need to.

Proactively calling your lender to ask about cancelling your PMI (if you see it on your home loan statement) can help lower your monthly payment.

The bottom line

There's many different things that can make up your monthly house payment.

- Association dues.

- Insurance.

- Principal.

- Interest.

- Taxes.

- PMI.

Making sense of these different things is the first step to saving money on your house payment.

If I was buying my first home again.

I'd be thinking about these 4 ways to save money:

1. Do I really need to have association dues? Or can I find a home with low or no association dues?

After getting a home loan, to try and save money I'd be thinking:

2. Am I getting a good deal on my homeowners insurance or should I shop around?

3. Can I pay a little bit extra on my home loan every month to save a lot of money in interest charges over the long run (which will also pay my loan off early)?

4. If I have PMI showing up on my home loan statement, I need to get rid of it asap by talking to my home loan lender (which may save me thousands of dollars per year).

These are four things I wish I learned more about earlier in my homebuying journey. Hope they're useful.

That's all for today.

See you next Saturday.