The 7 Steps to Buy a Home (without going broke)

Mar 21, 2026Read time - 4 minutes / Disclosure

Buying a home means:

- Becoming an owner.

- Owning your living space.

- Building generational wealth.

Unfortunately, homebuying can be a confusing thing.

The Journey

Buying your first home means finding:

- A loan officer.

- A real estate agent.

- A nice neighborhood.

And an affordable home.

There's a lot to consider.

Especially today when home prices are up.

And interest rates are up.

So how exactly does homebuying work?

And is it possible to buy an affordable home?

"The best investment on Earth is earth."

— Louis Glickman

Over a decade ago, I remember staring at the yellow walls in the small bedroom I was renting in Seattle, Washington.

Wondering if I should keep renting.

Or if I should figure out how to buy my first home.

I didn't know anything about homebuying.

And wasn't sure if I could get a home loan.

But after doing a little research.

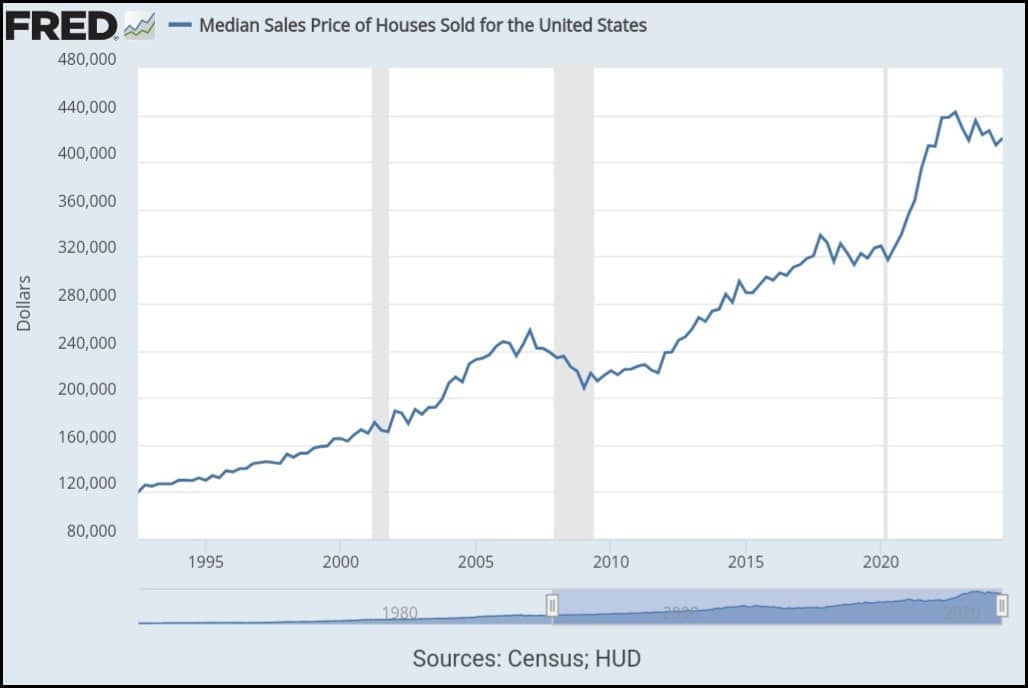

And seeing a chart like this of home prices going back several decades..

I figured buying a home was a good way to build wealth.

Finding a loan officer didn't take long.

And they helped me get a home loan to buy a tiny condo.

It was stressful figuring things out that first time.

Moving out of my small rental with the yellow walls and into the tiny condo..

Hoping I didn't make any big homebuyer mistakes along the way.

But watching the value of that tiny condo go up $100,000 in the first two years, shocked the heck out of me.

"The best time to buy a home is always five years ago."

— Ray Brown

Afterwards, I found myself obsessed with real estate.

So obsessed that I learned how to get 6 more loans to buy 6 more properties.

Figuring out how to buy a home without having to come up with a bunch of money became my weird obsession.

(because I didn't have much money starting off)

A few years into my real estate journey I found myself working as a banker for Chase Bank.

This helped me learn more about home loans and real estate.

The bank noticed my weird real estate obsession and had me teach over 40 first time homebuyer seminars the 10 years I worked there.

Watching someone's eyes light up the first time they realize it's possible to buy their first home never gets old.

After leaving my banking job and starting this little online education business (Millennial Wealth).

Many people have asked how buying their first home works.

And how to do it without needing to save up a boatload of money.

So here's a short little guide I wish I had when getting a loan to buy that first tiny condo.

The Homebuyer Roadmap

Here's the 7 steps to buy a home plus 4 ways to get first time homebuyer money.

Hope it's useful.

Let's dive in.

1. Deciding to Buy

For most people, I've found deciding to buy a home is often based on 2 things.

The 1st thing:

Asking yourself the question..

Do I want to own a home?

Owning a home means spending time and money on things like:

- Buying a new heater.

- Replacing a broken dishwasher.

- Calling a plumber to fix a plugged up toilet.

But buying a home also means:

- Owning an asset.

- Having a place to call home.

- Building generational wealth for your family.

There's pros and cons to consider when going from renter to homebuyer.

The 2nd thing:

Another question to ask yourself is..

Can I qualify to get a home loan?

According to the National Association of Realtors, 8 out of 10 people use a home loan to buy their first home.

Most people don't have $300,000+ in cash laying around (I sure didn't).

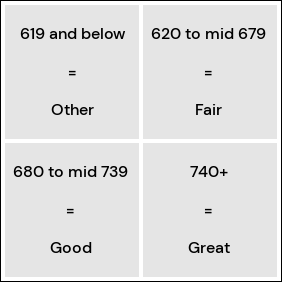

Getting a good deal on a home loan has a lot to do with a homebuyer's credit score.

Many home loan lenders view credit scores like this:

Credit score ratings

A homebuyer with a 740+ credit score.

Has a lot more home loan options than a homebuyer with a 619 or below credit score.

A score of 619 or below doesn't mean it's not possible to get a loan to buy a home.

It just means there's less home loan options available.

Wanting the responsibility of becoming a homeowner and having many home loan options are two big parts of the homebuying decision.

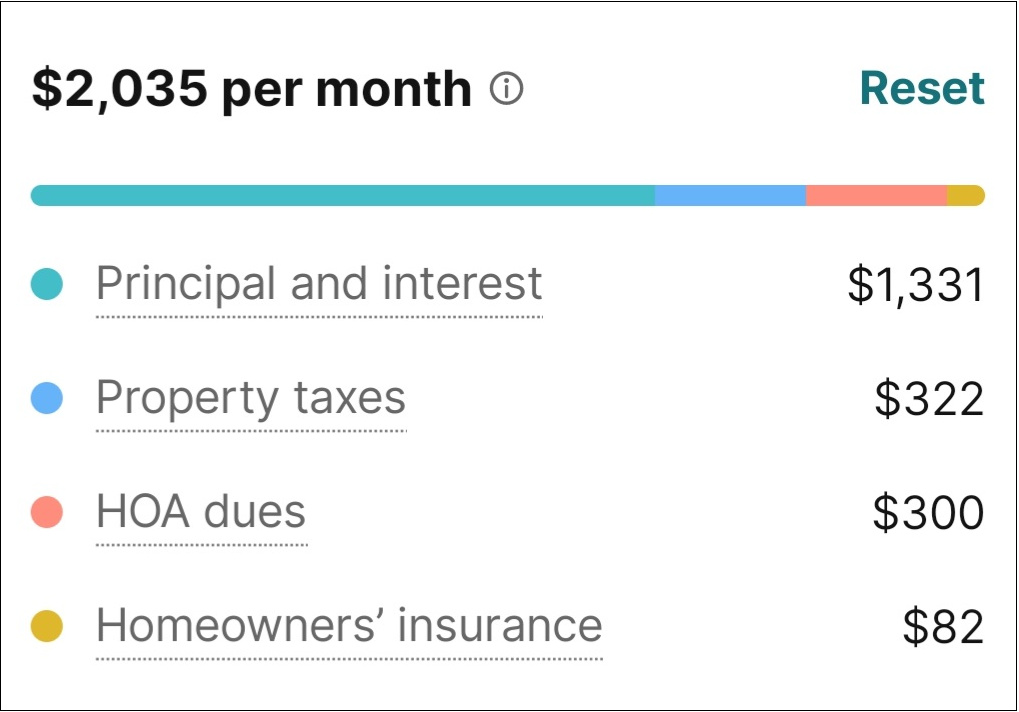

2. Determining Your Budget

Home loan payments can be more expensive than renting.

One way I've found to help keep my monthly costs down as a homeowner was to buy property with a separate area I could rent out.

For example:

Instead of buying a tiny 1 bedroom condo as my first home, I found a tiny 2 bedroom condo.

The purchase price was more.

But buying a 2 bedroom condo and renting out one of the bedrooms.

Was less expensive each month than buying a 1 bedroom condo and making the entire monthly payment all by myself.

This works with houses too.

For example, I lived downstairs in this home and rented out the upstairs:

The renter (my friend) and I each had our own separate living areas.

Later on, in this other home I rented out the garage and bedroom which are used as separate living areas as well:

Using this strategy can work too if you have a larger family.

Another option is to find a home with a tiny rental unit in the backyard.

Or putting one in yourself if you're a handyperson (Home Depot sells lots of tiny homes for the backyard).

I've found it helpful to keep these options in mind when looking for a home.

The free Redfin app has been my favorite way to look up homes for sale.

It has an easy to use calculator to estimate the monthly payment when looking at a home.

Renting out part of your home can lower your monthly payment by 25% to 40% (if you want) and free tools like Redfin can help you estimate your monthly payment in advance.

3. Getting a Home Loan

Applying for a home loan pre-approval means sharing your:

- Employment history.

- Bank statements.

- Tax returns.

- Paystubs.

...and other personal info with a loan officer.

The loan officer will review your info to figure out which type of home loan they can pre-approve you for.

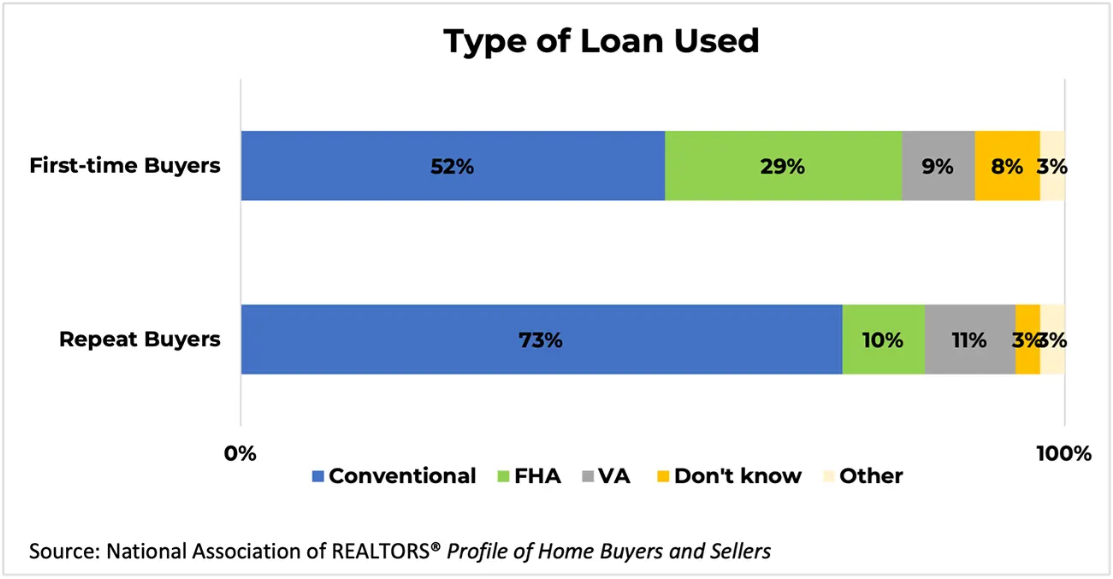

According to the National Association of Realtors, here are the 3 most common types of home loans:

And here's a short explanation for each type of home loan:

The VA Loan

VA loans are for service members of the military, veterans, and members of the national guard and reserve.

VA loans allow a down payment as low as 0%.

So if a home was selling for $400,000.

And a homebuyer qualifies for the VA loan.

They would not need to come up with any money for the down payment.

The FHA Loan

FHA loans are for everyone.

FHA loans allow a down payment as low as 3.5%.

So if a home was selling for $400,000.

And a homebuyer qualifies for an FHA loan.

They would need to come up with $14,000 for the down payment (more about where this money comes from below).

The Conventional Loan

Conventional loans are the most popular home loan.

Conventional loans allow a down payment as low as 3%.

So if a home was selling for $400,000.

And a homebuyer qualifies for the conventional loan.

They would need to come up with $12,000 for the down payment..

Coming up with down payment money.

Is often the hardest part for most first time homebuyers.

(it was the hardest part for me too)

The 5 most common places people get their down payment money from are:

- Investment accounts.

- Retirement accounts.

- Gift funds from family.

- Checking/savings accounts.

But the most overlooked option is:

- First time homebuyer programs.

There's over 2,000+ first time homebuyer programs in America that cover $5,000 or $10,000 or $20,000+ of a first time homebuyer's down payment.

(many of these programs are still offered even if you're not a first time homebuyer)

And there's a website that lists most of these programs:

→ access my free cheat sheet to help you find first time homebuyer programs here

Two things to remember when buying a home:

1. You have the down payment.

2. You have closing costs.

Closing costs are other fees that are part of buying a home.

For example:

- Escrow/Attorney fees.

- Government fees.

- Lender fees.

- Title fees.

But the good news..

Many first time homebuyer programs help cover these fees too.

(and there's several other ways to get homebuyer money we'll talk more about below)

Getting a home loan pre-approval and using first time homebuyer programs can help you buy a home sooner.

4. Shopping for Your Home

Finding and working with a real estate agent you trust can help you find your ideal home faster.

I've found Realtor.com to be a helpful free place to find local real estate agents and to read past customer reviews.

The free Redfin app has been my favorite way to lookup properties for sale the past 10 years.

It has other free tools I find useful too when looking at homes for sale, like:

- The local schools rating.

- The neighborhood score.

- The free notifications it sends when a new home is listed.

Having an experienced real estate agent, and using free home shopping tools can help you find a home faster.

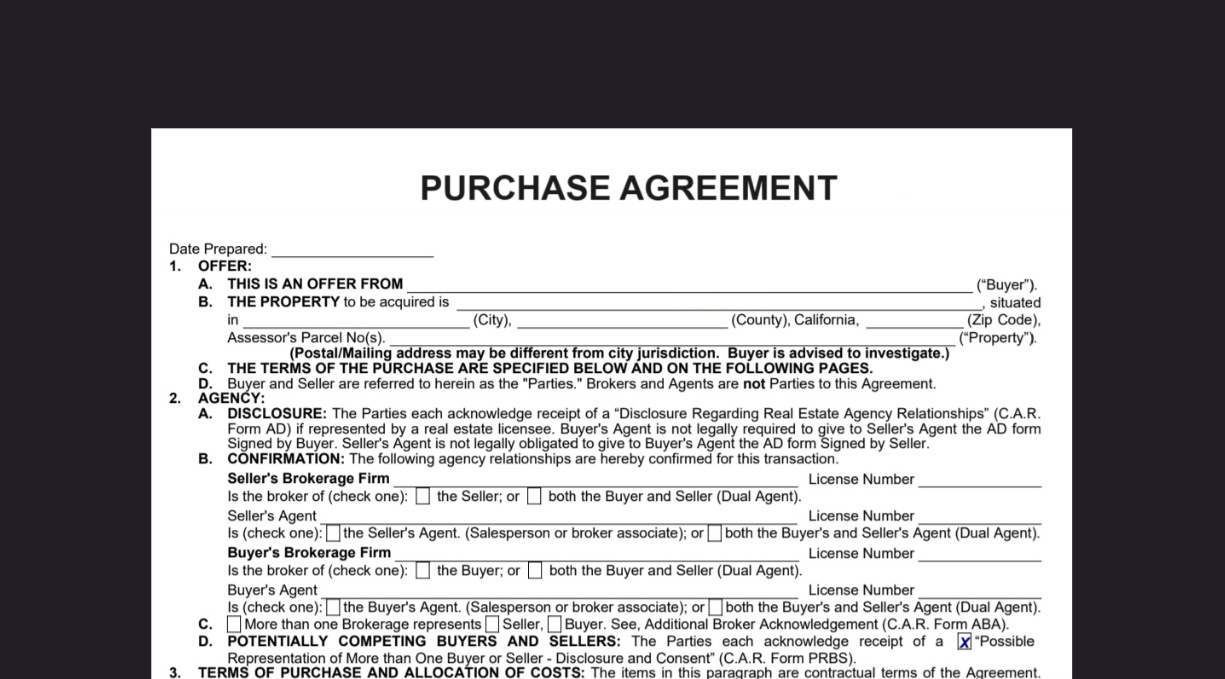

5. Making an Offer on a Home

After finding a home you love.

Your real estate agent will write up a purchase agreement on the home for you to sign before sending it to the real estate agent of the home seller.

The agreement includes things like:

- Your offer price.

- Any requests you have.

- Your home loan pre-approval letter.

- The date you want to become the new homeowner.

Example purchase agreement

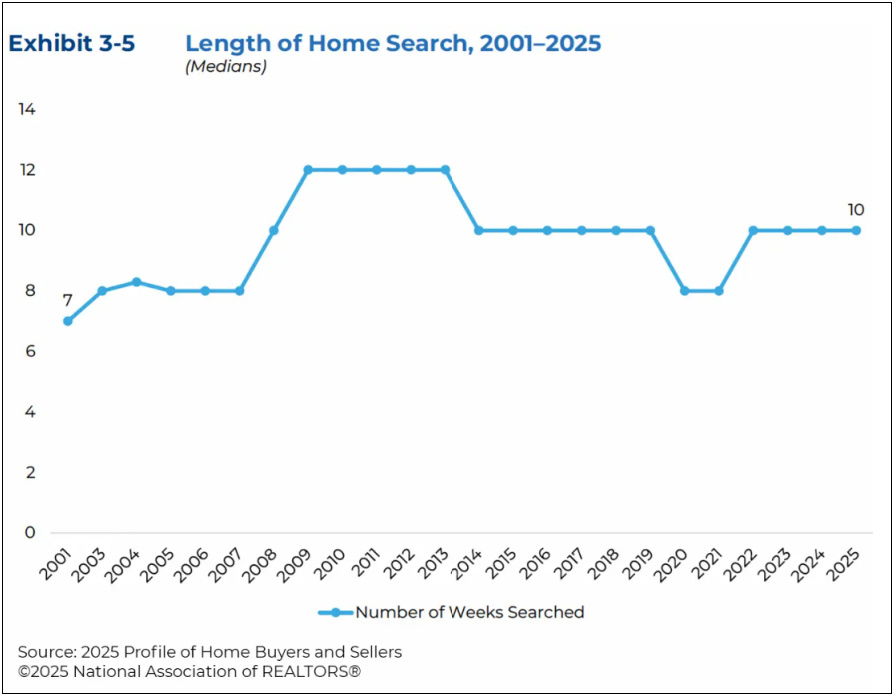

According to the National Association of Realtors, it takes most people 10 weeks on average to find their new home.

Thinking back to when I got a loan to buy my first tiny condo.

The one thing I wish I knew before home shopping.

Was all of the different ways to get first time homebuyer money (things nobody told me).

Here's 4 different ways to get homebuyer money:

→ access the free playbook I've used to get $30,000 when buying a home here

Knowing the different ways to get first time homebuyer money can help you buy a home sooner.

6. Preparing to Close on Your Home

After a home seller accepts your offer to buy their home.

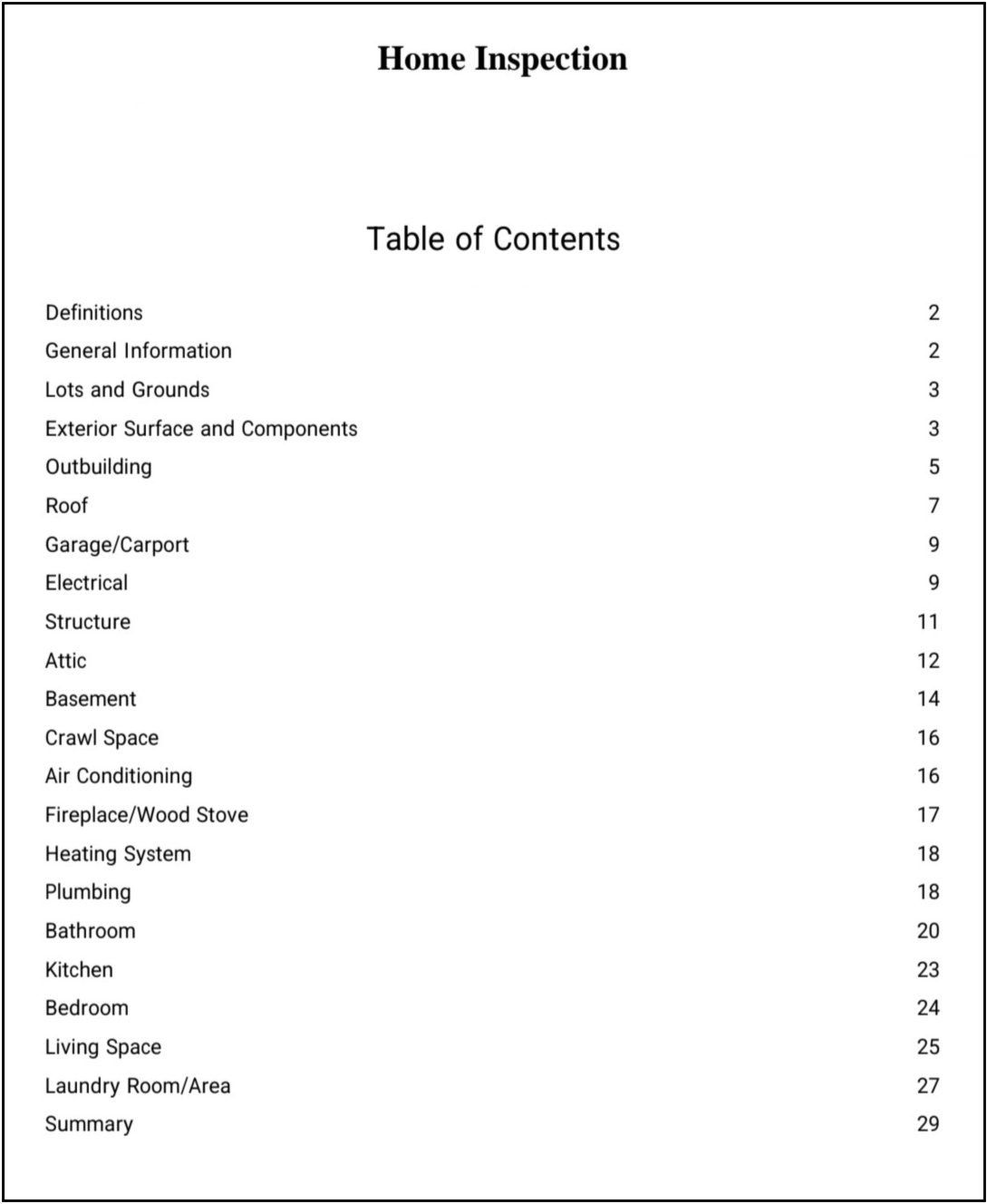

Many people do a home inspection.

A home inspector will come out to the home and inspect things like:

- The electrical system.

- The frame and foundation.

- The general quality of construction.

And you'll get a 25 to 50 page report that looks like this:

Some people only do a home inspection.

And some people do 2 or 3 different inspections like:

- A home inspection.

- A pest/termite inspection.

- A well inspection (if there's a well).

Inspections help you figure out if you still want to move forward with the purchase of the home after the home seller accepts your offer.

7. Getting Ready for Closing Day

If you're happy with the results of your home inspection.

Many people move forward with buying the home.

Which includes:

- Getting their final loan approval.

- Signing their home loan documents.

- And getting the keys to their new home.

After finalizing your home loan, moving into your new home is the last step!

The bottom line

There's many decisions to make when buying your first home.

It can be stressful.

But it can also be exciting to walk through different homes for sale and think..

"hmm, my couch can go here...the TV can go there...perfect, there's a Starbucks and a grocery store close by..."

(that's what usually goes on inside my mind anyway..)

Buying a home is a thrilling experience.

A new chapter of life.

If you see homebuying in your future.

I hope this mini guide is helpful.

Here's a little cheat sheet with the steps above and a timeline that might be useful too:

That's all for today.

See you next Saturday.