What to Avoid When Buying a Home (6 things to know)

Jun 27, 2026Read time - 4 minutes / Disclosure

Knowing what to avoid when buying a home can:

- Save you time.

- Save you money.

- Keep your homebuying goals on track.

Unfortunately, there's hidden mistakes along the way.

The Journey

According to the U.S. Census Bureau, 65% of homes in America are owner-occupied.

That means the odds of owning a home are pretty high for most people.

Which often means:

- Getting a loan.

- Shopping for a home.

- Making an offer on a home.

- Doing a home inspection.

- Closing on your new home.

There's many steps along the way.

Which can be stressful.

And exciting.

So, what should you avoid doing on your homebuying journey?

"A home is probably the most significant financial transaction most people will ever make."

– Warren Buffett

Looking back, buying my first home was a bit strange.

Joe the loan officer that helped me get a home loan asked for my:

-Paystubs.

-Tax returns.

-Bank statements.

...and a few other things.

Then, he gave me a loan pre-approval and told me what I could afford to buy.

Which wasn't much.

At the time, I was selling cell phones in a mall in Seattle, WA for Verizon.

But I gladly accepted the loan pre-approval.

And started looking at tiny condos (the only thing Joe said I could afford).

Soon after, I got a promotion at work from a cell phone sales guy to an assistant manager.

It felt like a big deal at the time as a young guy.

But when I told Joe, he wasn't happy.

The Promotion

After looking at my job offer.

Joe said he had to adjust my home loan pre-approval.

He said since my base pay was going up, and my commission pay was going down.

It would affect how much of a home loan I could get.

Which seemed confusing at the time.

But Joe gave me a slightly lower home loan pre-approval.

And shortly after, I found a home in my price range to buy.

The 6 Things to Avoid

After buying that first tiny condo.

And watching the value of it go up $100k in 2 years.

I found myself obsessed with real estate.

Joe helped me get 3 more home loans to buy 3 more properties in Seattle, Washington.

Then, I lost my job selling cell phones in the mall (actually I got fired when I was 29...oops).

And I then started working in finance.

After getting home loans to buy 7 properties, and watching hundreds of other people buy homes while working in finance.

Here's 6 things I've learned to avoid when trying to get a home loan.

Hope it's useful.

Let's dive in.

1. The New Car

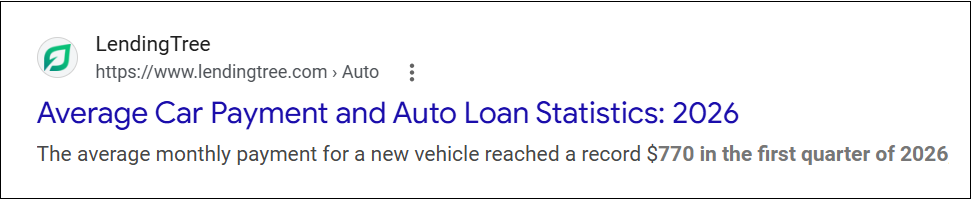

Getting a new car can kill the homeownership dream.

It's one of the largest payments most people have.

And they're not getting any cheaper.

Having a big car payment can make it harder to qualify for a home loan.

Avoid getting a new car payment (if possible) before trying to buy a home.

2. The Credit Card

Opening a new credit card can affect getting a home loan.

For example:

Dave gets a special offer from a credit card company.

0% interest for 12 months.

And Dave needs to buy furniture for his new home that he's closing on in 2 weeks.

So Dave opens the credit card and puts $5,000 worth of furniture on the card.

Soon after his loan officer calls in a panic.

And says they received a notification from the credit bureau that Dave just opened a new account.

And his new $150 monthly credit card payment was going to cause a problem with Dave getting his home loan.

Avoid opening and using a new credit card while buying a home.

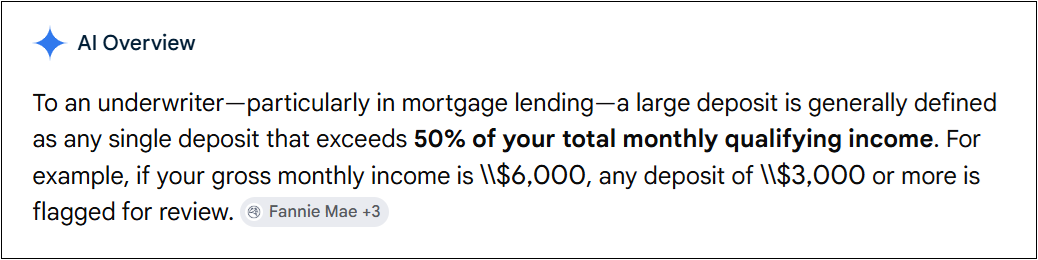

3. The Large Deposit

Large deposits can cause large problems.

When getting a home loan, a loan officer will look closely at your recent bank statements.

To make sure you have the money that's needed to close on your new home.

Things like:

- Money for closing costs.

- Money for a down payment (if required).

And large deposits showing up on a bank statement will be questioned.

But what exactly is a large deposit (A.I. does a good job explaining):

If a large deposit can't be explained with documentation to an underwriter (the person that approves your home loan).

That money can't be used to help buy a home.

For example:

Jennifer decides to have a yard sale.

And it's a big hit.

She deposits $5,000 cash into her bank account, the money she made from the yard sale.

Jennifer is also in the middle of buying a house.

And she plans to use that money to help with her homebuying costs.

But soon after, her loan officer notices the large deposit into her account.

And asks Jennifer to provide documentation showing where the money came from.

Jennifer can't show where the money came from because it was a cash deposit.

Her loan officer tells her that money can't be used to help buy her new home.

Avoid making large deposits (like cash) that can't be fully explained when buying a home.

4. The Career Change

Timing is everything.

When getting a loan to buy a home.

A loan officer will review many aspects of a homebuyers financial life.

And most major changes are questioned.

For example:

Scott's made good money working in marketing for 5 years.

One day, he decides he could make more money if he quits his job and starts working for himself.

So in January, he quits his 9-5 job and starts his own tiny marketing firm.

Over the next 6 months Scott finds himself making double the amount of money he was making working his 9-5 job.

And decides to get a loan to buy a house.

He talks to a loan officer at a bank and explains he quit his job 6 months ago.

But he's making more money as a self-employed person.

The loan officer explains, although he's in the same line of work.

He doesn't have any tax returns showing his self employment income because his business is new.

That he needs to come back after his business shows up on his tax returns.

Avoid making career or job changes right before buying a home (if possible).

5. The Loan Co-Signing

Co-signing can derail a homebuyer.

For example, co-signing for another person to:

- Get a car loan.

- Get a student loan.

- Rent an apartment.

And it's sometimes called different things.

Agreeing to be responsible for someone else's payments can make it harder to qualify for a home loan.

Avoid co-signing for someone else's debts (if possible) when you want to buy a home.

6. The Credit Card Usage

Using an existing credit card can be a problem.

For example:

Rachel talked to a loan officer and got a home loan pre-approval for $400,000.

Her loan officer told her to avoid opening any new accounts while shopping for her home.

And while shopping for her home, Rachel noticed Macy's had a watch on sale she wanted.

It was an expensive watch.

Rachel knew she wasn't suppose to open any new accounts.

So instead, she bought the watch using one of her existing credit cards.

A few weeks later when she was getting ready to close on her home.

Her loan officer called in a panic.

Saying when they did her home loan pre-approval.

That her credit card payment was just $25.

But now her credit card payment is showing up as $175.

And the higher credit card payment was causing a problem with Rachel getting her home loan.

Avoid adding big purchases to an existing credit card when buying a home.

The bottom line

This may feel like a lot of things to remember.

But the one big thing to remember right before getting a loan to buy a home is:

Don't do anything different.

Things like:

- A new car.

- A large deposit.

- A career change.

- A new credit card.

- Co-signing on a loan.

- Increasing the balance on an existing credit card.

Doing these things right before trying to get a loan to buy a home can make things harder.

I hope this little cheat sheet is useful if you see home buying in your future.

That's all for today.

See you next Saturday.