From $0 to $100k Invested (starting from scratch)

Mar 07, 2026Read time - 4 minutes / Disclosure

Going from $0 to $100k invested can:

- Lower your stress.

- Improve your mood.

- Give you more options.

Unfortunately, times are tough.

The Struggle

Most millennials and gen Z were told a successful life means:

- Going to school.

- Getting a good job.

- Working hard for 40 years.

And that leads to a fruitful retirement.

It's the path our parents took, and their parents.

And it worked well for them.

But many people following that path these days don't feel like they're getting ahead.

Groceries cost more.

Insurance costs more.

Raises at work are small.

Yet..

House prices are booming.

And the stock market is zooming.

"Wealth is assets that earn while you sleep."

— Naval Ravikant

At 29, I remember laying in bed eating a pint of Ben and Jerrys Ice Cream every night.

I was let go from my job and hadn't worked in 9 months.

To top it off, I had $50k in debt on my credit cards.

I was feeling sorry for myself.

And felt stuck.

Digging out of that hole felt impossible at the time.

But eventually life took a turn for the better.

I got hired at a bank.

And started learning more about money and investing.

Watching wealthy people manage their money over the next 10 years felt like a cheat code.

A cheat code that helped fix my $50k in credit card debt and helped me build better money habits.

Years later, in my 30s.

I found myself quitting my job as a banker at Chase Bank with $1M of investments.

Eager to start working for myself part time on this little online education business (Millennial Wealth).

Many people ask what I would do if I was starting all over again from scratch.

The Money Reset

Here's the 5 steps I'd take to get rid of my credit card debt and get to $100k of investments as quickly as possible.

Hope it's useful.

Let's begin.

1. The Money Guide

Using a money system is the first step I'd take to start fixing my finances.

When I had $50k on my credit cards.

I wasn't using a system with my money.

Each month I was just "winging it".

But doing that wasn't working.

So I started using a money guide like this one:

(you can access the free money guide I use here)

Using a system for just 30 minutes each month means having a plan for your money and helps get rid of money anxiety.

2. The Debt Avalanche

Many people struggle with getting out of debt (myself included).

The tool I found to be the most helpful is called The Debt Avalanche.

It works like this:

1. Make a list of all your debts.

2. Sort the list from highest to lowest interest rate on the debts.

3. Keep making all of your minimum monthly payments.

4. Focus on paying off your highest interest rate debt first.

For example:

If these were my credit card debts—

This is how I'd pay them off:

Credit Card 1

24% interest rate (pay 1st)

Credit Card 2

21% interest rate (pay 2nd)

Credit Card 3

19% interest rate (pay 3rd)

The Debt Avalanche method is a step by step plan that helps you save the most money when paying off high interest rate debt.

3. The Investment Picks

To keep things simple, I'd invest in 3 ways.

Way 1:

If my job offered a retirement account.

And they matched a certain amount of money I put into the retirement account.

I'd start putting money into that account right away (even while I was paying off my credit cards).

According to Fidelity Investments, most companies offering a retirement account match up to 5% of your annual income on average in your retirement account.

So if you're making $70,000 a year and put 5% of each of your paychecks into your retirement account.

And your employer matches that 5%.

That means your employer will put $3,500 per year into your retirement account.

($3,500 is 5% of a $70,000 annual salary)

I wouldn't want to pass up this "free money" even if I was paying off my credit cards.

The retirement match rules are a bit different with each employer.

So it's important to read through the details first.

Way 2:

After my credit cards were paid off, I'd open a 2nd investment account outside of work.

And I'd put the money that was going towards my credit cards each month (that are now paid off)..

Into the new investment account each month.

The money would invest in an S&P500 fund like VOO (The Vanguard S&P500 Fund).

I'd invest my retirement account money at work in an S&P500 Fund too (most retirement accounts have this option).

Investing in an S&P500 fund means investing in the 500 largest companies in America which include:

- Apple.

- Google.

- Amazon.

- Microsoft.

- Mastercard.

+ 495 other companies.

Money invested in an S&P500 fund has been doubling in price every 8 years on average since the 1990s as America's largest companies continue to grow:

Stock market history: the s&p500

Way 3:

I'd start working with a loan officer to figure out how I could qualify to get a home loan to buy real estate.

But I would make sure the loan officer knew I was planning to get a lot of homebuyer money so I wouldn't have to spend years saving up a bunch of money.

(you can access the playbook I use to get $30,000 in homebuyer money here)

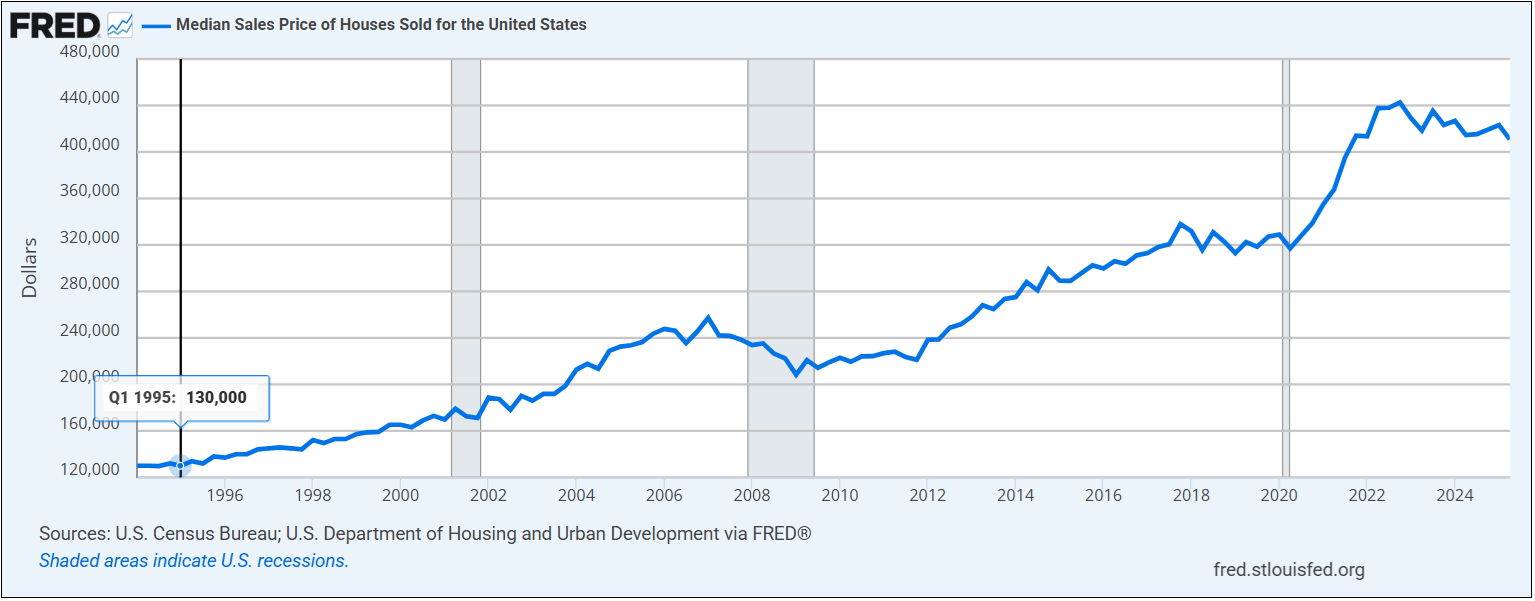

The price of a home has been doubling every 14 years on average since the 1990s:

Real estate history

To avoid making a big home loan payment every month all by myself.

I'd find a home with a separate area I could rent out.

Like a 2 bedroom condo.

Or find one of these homes:

3 Homes That Pay You (what to look for when buying)

Learning how to get homebuyer money and getting loans to buy homes with separate areas I could rent out is how I was able to buy 7 properties starting from scratch.

The stock market and real estate are the 2 most common ways people invest.

4. The Easy Mode Approach

Automating my investments would be next.

Planning to invest when there's "extra money" each month..

Doesn't work very well.

I've tried it.

Money in a checking account somehow always manages to get spent (or maybe it's just me).

What I've found works better..

Is to have each paycheck go into different accounts like this:

1. Part of each paycheck would go into my retirement account at work.

2. Part of each paycheck would go into the investment account I opened.

3. Part of each paycheck would go into my savings account for buying a home.

And the rest would go into my checking account.

"Before you pay your bills, before you buy groceries, before you do anything else, set aside a portion of your income to save."

"The first bill you should pay each month should be to yourself."

— J.D. Roth

Most employers will deposit your paycheck into different accounts if you login to your employee website at work and make those changes.

Automating your savings and investments makes things easier and makes sure these important things happen.

5. The Double Down Investor

After helping over 20,000+ people while working in banking for 10 years.

I watched all of the different ways people try to save and invest more money.

So I created a list of the many different ways:

(you can access the cheat sheet I use to save and invest more money here)

Saving and investing hundreds or thousands of dollars per month means getting to $100,000 of investments much faster.

The bottom line

After years of helping other people with their money.

And figuring out my own money troubles.

I've noticed there's 2 big things when it comes to money success.

Thing 1:

Knowing what to do.

And..

Thing 2:

Actually doing it.

What most people struggle with is Thing 2.

Finding the motivation:

- To save money.

- To invest money.

- To keep doing it each year.

It's also something I struggled with.

And the best way I found to motivate myself to do these things before leaving my 9-5 job was to think about:

1. The day I'd tell my boss I was quitting.

2. The places I was going to travel because I no longer needed a 9-5 job.

3. The work I was going to do part time for myself after quitting my job because I still wanted to have a purpose in life and make money...but at a slower pace.

Thinking about these 3 things helped fire me up to do the things I needed to do with my money so I could leave 9-5 life early..

Even when I didn't feel like doing them.

So if you've ever struggled to find the motivation to deal with your money (like me).

I'd suggest this.

Imagine walking into your bosses office Monday morning with a sheepish grin on your face.

And telling him or her that you've decided to quit.

That working a 9-5 job for 40 years of your life is not for you.

That you've already built up enough investments that you've decided to just work part time for yourself.

That you can only work 2 more weeks because you've decided to celebrate this new chapter of your life by..

- Taking a month long vacation in Hawaii.

- Then taking a 2 week cruise through the Mediterranean.

- After that, taking a 3-week trip visiting different countries in Europe.

Then you'd come home, rest and start working for yourself part time doing something you love.

Maybe it's a little online business.

Or maybe it's spending 10 hours per week teaching people something you're good at doing.

Imagining these things motivated the heck out of me to get my money right.

To focus on investing.

To plan for a freer future this decade, not when I'm in my 60s.

I hope this little imaginary hack works for you as well as it worked for me if you need a bit of money motivation.

That's all for today.

See you next Saturday.